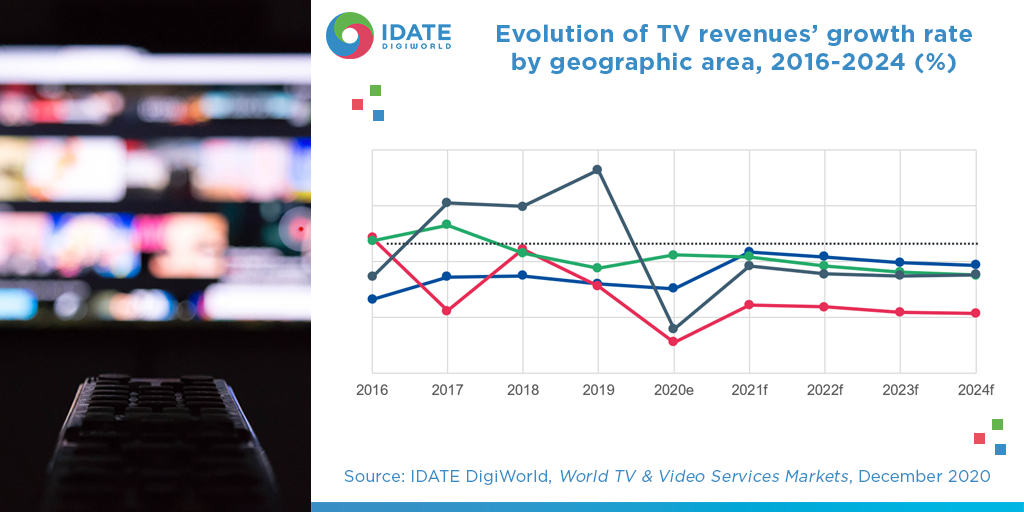

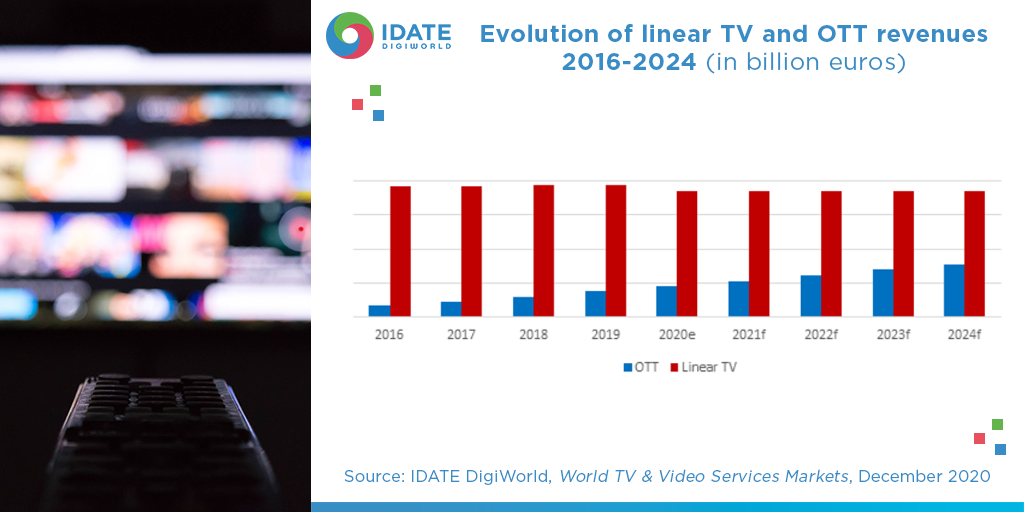

The Covid-19 crisis further propelled the TV market’s downward trend. Over the long term, this can be attributed to the pay-TV market’s decline, but the drop in TV ad revenue has only aggravated the situation. North America and Western Europe are the hardest hit, while it is countries in the southern hemisphere and Asia that are driving the market forward. Fortunately, the OTT sector’s healthy momentum is more than offsetting this decline. It is expected to represent a third of the TV and video market’s revenue in 2024.

Our TV and video market observatory delivers detailed figures and an analysis of the driving trends, along with a dataset and concise summary report.

It covers the latest developments in 38 countries and 12 regions and sub-regions, along with a consolidated global snapshot.

The dataset provides figures back to 2016 and forecasts up to 2024 for the key indicators used to track the TV and video sector.

The report provides an analysis of the main market trends and the developments to watch in the coming months and years.

Key Figures:

- The COVID-19 crises only aggravated the TV market’s downward trend: linear TV revenues fell by 4% in 2020.

- The audiovisual market value has been steadily shifting from veteran TV players to the Internet giants: OTT’s share of total TV/Video revenue is estimated at 29.4% in 2024.

- Advertising and subscription provide 90% of the audiovisual sector’s financing.

Access the study

World TV & Video Services Markets