The Internet has introduced major changes to the way content is distributed, to the way games are played, to business models and even to how video games are developed. These changes are also building bridges between market segments, leading to more open platforms, more platform convergence, more uniform business models, and more ubiquitous content and consumption patterns.

Online games enhance the gaming experience and create value: multiplayer games extend product lifecycles; downloadable content (DLC) and in-game purchases are becoming more widespread; community and social features are increasingly popular and essential.

Value chains are reforming: physical links are disappearing, revenue streams are being redistributed, and the position of developers and publishers – the content providers – is being revalued.

Since the end of 2013, major video games have all been dematerialised and distributed via console manufacturers’ digital stores.

The features of fixed and mobile devices are converging: in March 2017, we saw the perfect illustration of this convergence with the launch of the Switch, Nintendo’s latest console. It can be used as a handheld console, but once it’s connected to a docking station connected to a TV, it can be used as a home console.

Through games, there is starting to be some interoperability between consoles from different brands, something that was inconceivable three years ago.

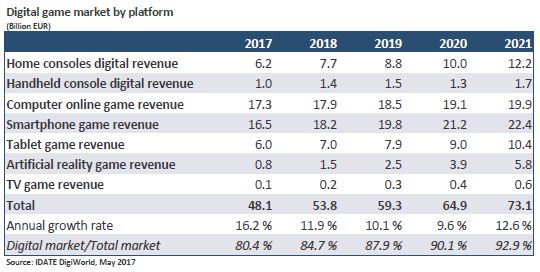

The digital proportion of the video game market should reach 48.1 billion EUR in 2017, which is 80% of the total market. By 2021 this proportion is likely to hit 92.9%.

In this environment, mobile games – especially smartphone games – have become the top video game market segment in terms of value. Its value chain is dematerialised from end to end; content is accessible at all times as long as there is a mobile telecommunications network; the user experience is very high quality thanks to high-performance devices; and the business models and prices are attractive.

China is gradually establishing itself as one of the leading video game markets thanks to its investment in the online and mobile segments with revenue close to 10 billion EUR.

To delve deeper on this theme

Check out our last DigiWorld Watch report

More info