Overall, the telcos are going through a tough period, where most KPIs are showing a negative growth trend. Subscriber numbers and thus overall revenues are continually growing, albeit slowly, but the revenue generated per subscriber is decreasing, while EBITDA continues to be squeezed and CapEx spending obligations increase. European telcos in particular are having a hard time, with both internal competition (against other telcos) and external competition (against OTTs) taking its toll.

As for the OTTs, the GAFAM and BAT dwarf the other Internet players in both absolute value and growth. These eight players generally show a steady and positive trend, but the other OTTs tend to be highly volatile and do not show a coherent pattern in their KPIs, demonstrating that for the majority the Internet service market remains far from mature.

As regard KPIs, a 30% EBITDA margin is often used as a measure to see if a given telco is able to sustain its business. 2015 EBITDA shows the telcos clustered at just over 30%, hence showing that the telcos are maintaining sustainability… just. The BAT all show much higher EBITDA figures in comparison, but the surprise here is Facebook, which also has a high figure at 46%. Elsewhere, Google and Facebook show similar values to the telcos, while Microsoft and Amazon have a rather low figure of just 8%.

An interesting observation in the CapEx is that all OTTs, both GAFAM and BAT, have lower CapEx ratios compared to the telcos (although Google and Facebook do have ratios close to the telcos). This supports the long-standing argument of the unfair playing field, where telcos are heavily regulated and required to invest substantially to maintain their infrastructures while this is not the case for OTTs. It is also interesting to note that European telcos are among the highest for CapEx ratios, which may have played a part in the EU announcing plans to ease current regulations to try and make the playing field more even. It is the Chinese telcos that have the highest CapEx however, demonstrating the nation’s current momentum.

The FCF is influenced by CapEx, so it is perhaps no surprise to see that the Chinese telcos score very low with 3%. At the other end of the scale the BAT scores very high, while the GAFAM can again be split into Google, Apple and Facebook who score relatively high (in between telcos and BAT) on the one hand, with Amazon and Microsoft scoring low on the other.

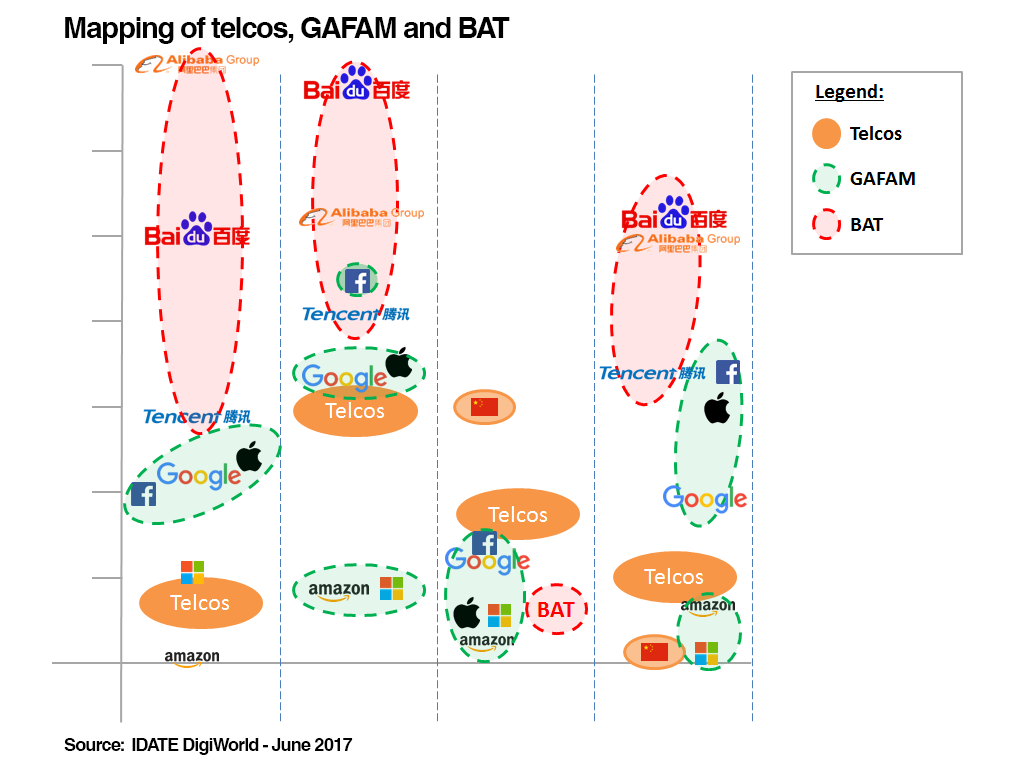

Looking at the market capital, the figures show that both GAFAM and BAT are valued higher than telcos with respect to revenues earned. When comparing GAFAM with the telcos, despite having similar revenues GAFAM have a significantly higher market cap. Also when comparing BAT with the telcos, the BAT has market capital comparable to the telcos despite having lower revenues. Thus the future is being seen as in the hands of the OTTs, GAFAM in particular, rather than the telcos.

Finally, concerning revenues per user, overall the OTT players generate lower revenue per head compared to telcos, in line with the general OTT philosophy of “increase users first, monetize later”. The only exceptions are Apple, which is first and foremost a device vendor with 90% of revenues coming from device sales rather than Internet services, and Amazon, which has successfully deployed e-commerce and cloud (AWS) services which generate stable revenues.

To delve deeper on this theme

Check out our last report

More info